Banks are rethinking how they serve customers, expanding from their onw products and services to become a convinience help to its customers. It a clever way to raise the preceved value of a bank, departing from a simple commodity, but it requires partners to come onboard.

They are experts in their field of business and bring experience and knowledge to the bank, while providing underlying services. And how you, has a bank leader can work with them?

Let’s start a series of posts about that.

1. Rethinking the Bank’s Role in the Consumer Value Chain

In today’s financial ecosystem, banks are evolving from being pure financial intermediaries to becoming lifestyle enablers. “Beyond banking” initiatives extend the bank’s value proposition into adjacent verticals like mobility, housing, education, and commerce — wherever customers interact with money.

One of the most promising models in this transformation is the e-commerce partnership. Here, a bank collaborates with an online retail platform to allow customers to buy electronics or other goods at preferential prices. The bank monetizes this new channel through commissions and customer engagement, while the partner leverages the bank’s client base and trust network to scale its sales and negotiate bulk deals.

Let’s consider a case where a bank has partned with a ecommerce provider to offer electronic produts to its customers.

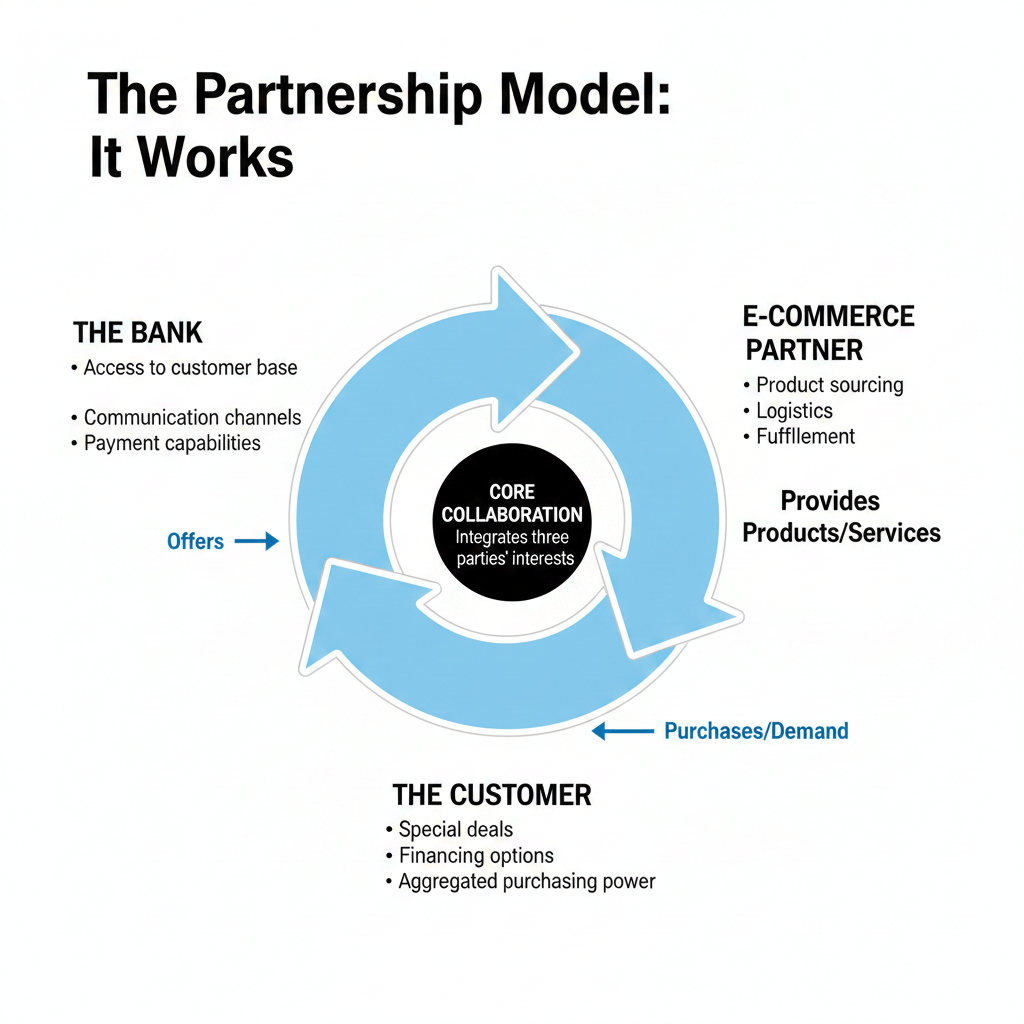

2. The Partnership Model: How It Works

At its core, this collaboration integrates three parties’ interests:

- The Bank provides access to its customer base, communication channels, and payment capabilities.

- The E-Commerce Partner manages product sourcing, logistics, and fulfillment.

- The Customer enjoys special deals or financing options, made possible by aggregated purchasing power.

- Customers access the partner’s shop via the bank’s app or digital banking platform.

- The e-commerce platform aggregates all customer orders and combines them with its existing supplier negotiations.

- Bulk purchasing reduces costs, enabling special prices for bank clients.

- The bank earns a commission on each transaction and strengthens customer loyalty.

3. Key Management Dimensions of the Project

a. Strategic Alignment

Ensure that the initiative aligns with the bank’s digital transformation and brand positioning.

The “beyond banking” partnership should reinforce trust and convenience — not shift the bank’s image toward retail competition, neither should be a superapp build. All greate suerapp are the result of a powerfull integration and ecosystem that, let’s be honest banks are not very good at..

b. Governance and Partnership Structure

Define clear roles and responsibilities from day one:

- Who owns the customer relationship?

- How is data shared and protected?

- What are the rules of engagement during promotions or high-volume campaigns?

Establish a joint steering committee and use agile governance to adapt to evolving requirements quickly.

c. Customer Experience Integration

The customer journey must feel seamless:

- Access from within the mobile banking app (via SSO or white-label integration)

- Consistent branding and communication tone

- Clear post-purchase support channels

Designing the journey jointly with CX experts from both entities is crucial.

d. Technology and Data Integration

Data privacy and security sit at the center. Integration typically includes:

- Secure API connections for session management and payments

- The buy interface can bem a website, embebed or API provided, it depends on your need, time/money available to put the project online.

- Data anonymization for analytics and offer personalization

- Shared dashboards tracking key KPIs: conversion rates, cart activity, and NPS

e. Commercial and Commission Model

A transparent financial model ensures alignment. Typical structures include:

- Revenue-sharing commission: a percentage of each completed sale goes to the bank

- Tiered bonus incentives: based on sales volume or customer activation milestones

- Marketing budget co-funding: both sides invest in digital campaigns through the bank’s channels

f. Compliance and Risk Management

Since banks operate under strict regulatory scrutiny, all promotional and transactional flows must comply with consumer protection, AML, and data-privacy guidelines. Early legal involvement avoids project delays later.

4. Measuring Success

Beyond short-term sales, measure long-term impact through:

- Customer activation: number of clients engaging with the new service

- Increased card/payment usage

- Cross-sell potential: linking purchases to financing, insurance, or subscription offers

- Customer satisfaction and retention

A true beyond banking project transforms transactional relationships into lifestyle engagement.

5. Lessons from Early Implementations

Successful partnerships share common traits:

- A minimum viable partnership (MVP) launch within a few months, followed by iteration

- Strong CX alignment — customers trust offers because they come from their bank

- Continuous co-marketing and communication synchronization between bank and partner

- Measured rollout to ensure operational and reputational readiness

Conclusion: Banking Beyond Transactions

E-commerce partnerships are not just an additional source of income for banks; they represent a significant shift towards ecosystem banking. By integrating lifestyle benefits into the financial experience, banks can create new value for their customers and position themselves at the core of daily digital life.

The winning strategy involves careful project management, aligned incentives, and a design focused on the customer. When executed effectively, it’s a win-win situation: customers save money, partners increase their sales, and banks enhance engagement and build trust.